Inflation hedges: Is fine wine the new gold?

Gold has traditionally been viewed as a ‘safe haven’ during periods of inflation, but fine wine outperformed during the 2021 inflation spike.

Gold is not always what glitters

We’ve written before about rising inflation and how fine wine can benefit an investment portfolio. Traditionally, gold is also thought of as a good investment to hedge against the negative impacts of inflation due to its status as a scarce real asset upon which society has valued for centuries. Gold has certainly performed very well in recent weeks amid the spike in uncertainty stemming from the conflict in Ukraine.

However, the current period of high inflation stretches back in the first half of 2021, and gold’s performance last year took some shine off its track record. Gold prices sank by -3.64% in 2021 (USD/ounce) while inflation surged. In the US, consumer price index (CPI) inflation rose 7.0% over 2021, the largest 12-month jump since 1982. In the UK, CPI prices rose by 5.4% – the highest increase since the Office of National Statistics’ records began in 1997. The OECD’s data across all G-20 economies shows CPI rose 6.1% over the 12-months through December.

Inflation decreases the purchasing power of money as well as the value of an investors’ portfolio. This makes gold’s negative performance in 2021 even lower in real (inflation-adjusted) terms. Gold does have some notable wins during periods of high inflation, such as the 1970s, but over long periods, gold may not always offer the best option.

Fine wine’s consistency

While gold stumbled in 2021, fine wine surged to record highs. The Liv-ex 1000 index, the broadest measure of the market, ended the year up 19.08%, keeping its real returns comfortably in positive territory. Using the G-20 CPI inflation rate, the Liv-ex 1000’s real return sat at 12.23% in 2021[1].

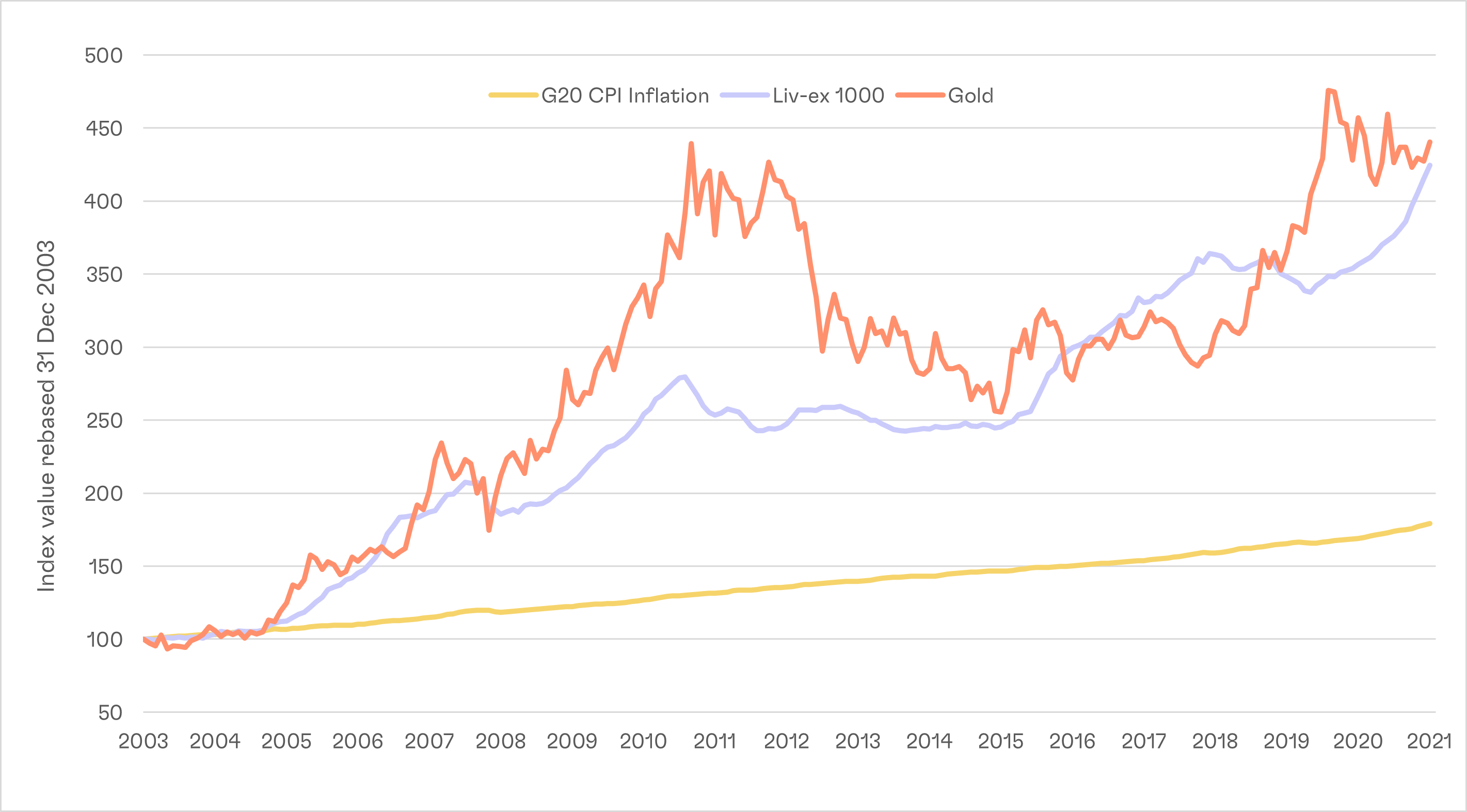

This wasn’t just a short-term blip, either. The below graph illustrates how fine wine’s performance in 2021 has helped keep its return easily above the inflation rate in G-20 economies since the inception of the Liv-ex 1000 index in January 2004.

[1] Source: Liv-ex as of 17 February 2022, analysis by Cult Wine Investment. Past performance is not indicative of future returns.

Fine wine’s strong and steady real returns

Liv-ex 1000 and Gold vs OECD’s CPI index (G-20 economies) since 2004

Source: Fine wine data from Liv-ex as of 31 Jan 2022; the performance was calculated in GBP and will vary in other currencies.

Gold price data from goldprice.org; performance calculated as USD/ounce and will vary in other currencies. Past performance

is not indicative of future returns.

Fine wine’s credentials versus gold

Stability

While gold has also outpaced inflation since 2004, it came with a noticeably higher degree of volatility than fine wine. The Liv-ex 1000 experienced a 4.94% standard deviation of monthly returns through the end of 2021, well below gold’s 17.07% over the same period2.

This stability is important; fine wine has been more likely to maintain its upward trajectory during different market environments – including rising inflation – compared to gold. Even if wine prices do not always spike every time inflation leaps higher, they offer a reliable track record of positive real returns.

Scarcity

Fine wine’s investment potential stems from its scarcity, similar to gold. Fine wine supply levels are constrained as only specific vineyards in certain regions have the necessary qualities and recognition to produce top quality wines. This can help support prices even as inflation weakens the purchasing power of hard currency.

Market drivers

Internal factors are the primary drivers of fine wine prices, including supply/demand, wine quality and brand prestige. Gold, meanwhile, is widely seen as a safe-haven asset during economic downturns and financial market selloffs (such as the current volatility). Therefore, mainstream market direction can exert a more direct influence on gold prices.

For example, the soaring equity markets in 2021 have been widely cited as a factor in gold’s negative performance, as investors moved back into risk assets even as inflation increased. Meanwhile, fine wine prices kept rising on the back of the internal supply-demand imbalance.

These traits do not mean fine wine will always provide a hedge during an inflationary backdrop or even always outperform gold during these times. In our opinion, we think fine wine’s track record and unique characteristics make it an investment for all seasons. Rather than increasing or decreasing exposure to fine wine depending on the prevailing inflation outlook, we believe fine wine can form a permanent component of a portfolio with the potential to deliver positive returns through shifts in inflation and other macro conditions.

* Past performance is not indicative of future success; the fine wine performance was calculated in GBP and will vary in other currencies. Any investment involves risk of partial or full loss of capital. The Cult Wine Investment Performance is a hypothetical tool. The results depicted here are not based on actual trading and do not account for the annual management fees that may be charged to a Cult Wines customer which ranges from 2.95% to 2.25% depending on the size of the portfolio, and there is no guarantee of similar performance with an investor’s particular portfolio.